Before you sign a contract that reduces your grocery budget for months, explore these Canadian-specific support systems. From Rent Banks that keep you housed to Utility Grants that keep the lights on, help is available without the debt trap.

When Does a New Loan Make Things Worse?

If you are on a limited income, every dollar counts. Borrowing is dangerous when:

- You borrow for essentials: If you use a loan to buy food, you will have even less money for food next month when the repayment starts. This is the “Payday Trap.”

- You borrow to pay other debt: Using a 47% interest loan to pay a 19% credit card bill is a mathematical mistake that leads to insolvency.

Instead of debt, look for Grants and Assistance.

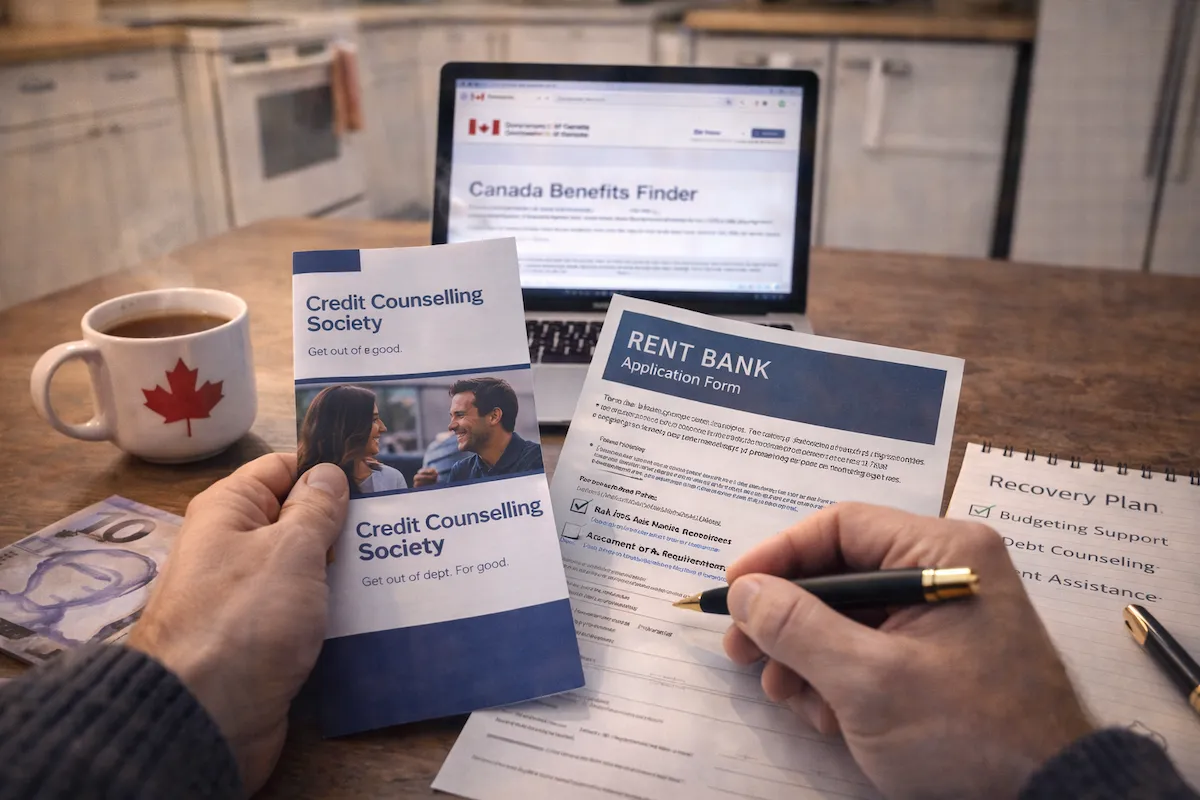

1. Rent Banks (Keep Your Home)

If you are behind on rent, do not go to a loan shark. Go to a Rent Bank.

What are they?

Rent Banks in BC, Ontario, and Manitoba offer interest-free loans or legitimate grants to low-to-moderate income tenants to pay rent arrears or utility deposits.

- BC Rent Bank: Offers interest-free loans to prevent eviction.

- Toronto Rent Bank: Provides grants to eligible residents (you don’t pay it back).

- Manitoba Rent Relief Fund: Provides interest-free loans for housing stability.

Action: Dial 2-1-1 to find the nearest Rent Bank program in your city.

2. Emergency Utility Help

In Canada, you have rights when it comes to heat and hydro.

Ontario: LEAP & OESP

If you are behind on your electricity or gas bill in Ontario:

LEAP (Low-Income Energy Assistance Program): Provides a one-time emergency grant of up to $500 ($600 for electric heat) to pay off arrears.

OESP (Ontario Electricity Support Program): Gives you a monthly credit on your bill to lower your costs permanently.

Alberta & Other Provinces

Alberta offers the Utilities Consumer Advocate mediation, and specific Emergency Needs Allowances can cover utility arrears if disconnection is imminent.

3. Free Financial Advocacy

You don’t have to fight creditors alone. Non-profit agencies can help you for free.

Credit Counselling Society & Credit Canada:

These are non-profit organizations (not lenders). They can:

- Call your creditors to stop interest.

- Put you on a Debt Management Program (DMP) to consolidate payments.

- Help you budget your benefits effectively.

The 7-Day Stabilisation Plan

If you have $0 in your account today, follow this plan instead of applying for a loan:

Day 1: Call 2-1-1

This is Canada’s primary helpline for government and community services. Ask for “Emergency Food” or “Housing Help.”

Day 2: Use a Food Bank

Visiting a food bank for one week saves you $100-$150 at the grocery store. Use that cash to pay your most urgent bill.

Day 3: Negotiate

Call your hydro or internet provider. Ask for a “Payment Plan.” They often allow you to spread a bill over 3 months if you ask before they cut you off.

Day 4: Unlock Benefits

Log in to your CRA My Account. Ensure you aren’t missing any GST/HST credits or Trillium benefits (Ontario). File your taxes immediately if you haven’t—this is how you get your benefit money.

Conclusion: Help is Available

Canada has a strong safety net for low-income residents, but you have to know where to look. By using Rent Banks and utility grants, you can solve your immediate crisis without handing over your future income to a lender.

For more details on navigating loans if you truly have no other choice, return to our guide on Loans for Low Income in Canada.