Myth vs. Reality: Borrowing on Benefits

Let’s clear up the confusion immediately.

Myth #1: “Benefits don’t count as real income.”

Reality: False. For alternative lenders (like Fairstone, easyfinancial, or Cash Money), benefits like the Canada Child Benefit (CCB), Canada Pension Plan (CPP), and Disability Support (ODSP/AISH) are considered valid, stable income sources.

Myth #2: “Lenders can’t take my benefit money.”

Reality: Complicated. While creditors generally cannot garnish government benefits at the source (before they reach you), once that money hits your bank account, it is just “cash.” If you signed a Pre-Authorized Debit (PAD) agreement, the lender has the legal right to withdraw payments from your account, regardless of where the money came from.

Myth #3: “I am guaranteed approval because my income is guaranteed.”

Reality: Dangerous lie. Just because your income is stable doesn’t mean you can afford a loan. If your rent and food costs eat up 90% of your benefit cheque, a legal lender must decline you.

Which Benefits Do Lenders Actually Accept?

Not all government cheques are created equal. Lenders prefer “permanent” or “long-term” benefits.

Widely Accepted (The “Green Light”):

- Canada Child Benefit (CCB): Highly trusted because it continues until the child turns 18.

- CPP & OAS (Pensions): Considered the gold standard of fixed income.

- Disability (ODSP, AISH, PWD): Generally accepted, as it is long-term.

Harder to Approve (The “Yellow Light”):

- Employment Insurance (EI): Lenders are cautious because EI has a strict end date. If you only have 2 months of EI left, you won’t get a 12-month loan.

- Social Assistance (Ontario Works/Welfare): Often declined by installment lenders because the amounts are typically too low to support loan repayments after living costs.

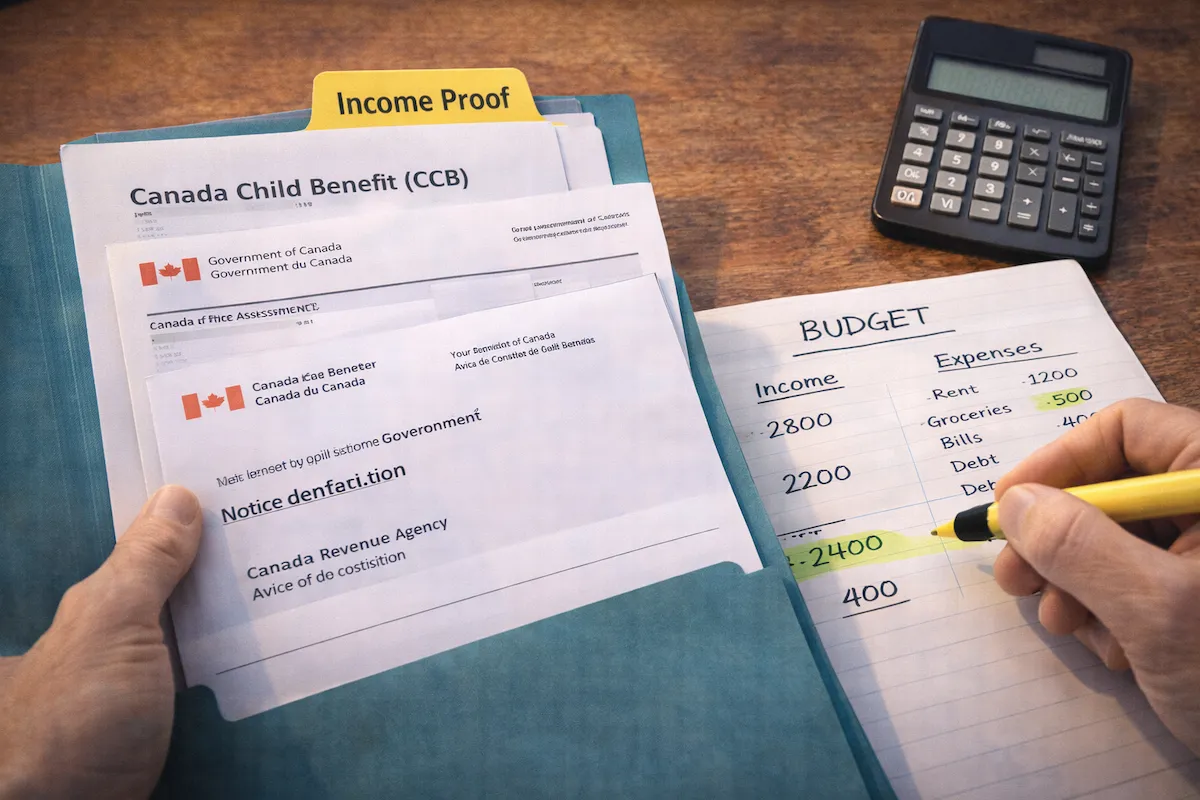

The Approval Rule: It’s All About “Surplus”

Lenders don’t just look at what comes in; they look at what goes out.

The Calculation:

Lenders calculate your Uncommitted Monthly Income.

Example: You receive $2,000/month in benefits.

– Rent: $1,200

– Food/Bills: $600

Surplus: $200

If your surplus is only $200, a lender cannot responsibly give you a loan with a $300 monthly payment. This is why many applications are declined—not because of the income source, but because of the income amount.

Why “Easy Approval” is Risky

If a lender promises to ignore your expenses and approve you anyway, be extremely careful.

- Predatory Rates: They are likely charging maximum allowable interest (or illegal rates).

- The “Cycle”: They know you can’t afford the payment, so they expect you to “re-borrow” next month to cover the hole in your budget. This traps you in debt forever.

Conclusion: Know Your Numbers

You can get a loan on benefits in Canada, but it requires honesty about your budget. Before applying, calculate your own surplus. If you have $0 left at the end of the month, a loan isn’t the solution—it’s a trap.

For a deeper dive into safe borrowing options, read our main guide on loans for low income and benefit recipients.